import numpy as np

import pandas as pd

import yfinance as yf

import matplotlib.pyplot as plt

import seaborn as sns

import statsmodels.formula.api as smf

import warnings

warnings.simplefilter(action='ignore', category=FutureWarning)

coins = ['BTC-USD','ETH-USD','LTC-USD','XRP-USD','DOGE-USD','BCH-USD','XLM-USD']

df = (

yf.download(coins, start='2015-01-01', progress=False)['Close']

.resample('ME')

.last()

.pct_change()

.dropna()

)

df.columns = [c.replace('-USD','') for c in df.columns]A Market Index for Cryptocurrencies

Introduction

Main purpose in this notebook:

- Apply what we just learned about model fitting and interpretation in a real finance setting.

- Build a crypto market factor (

MKT) and use regressions to separate common market exposure (beta) from coin-specific risk (R^2 gaps). - Compare crypto-market returns with stock-market returns (

SPY).

Core model: one-factor return decomposition for each coin i. r_i = \alpha_i + \beta_i r_{\text{MKT}} + e_i.

Interpretation:

- r_{\text{MKT}}: common crypto market shock (systematic component).

- \beta_i: sensitivity of coin i to that common shock.

- \alpha_i: average return component not explained by the factor.

- e_i: idiosyncratic component (coin-specific variation).

Why this model is useful:

- It decomposes returns into common risk vs coin-specific risk.

- It gives a compact way to compare coins with two summary statistics:

Betafor sensitivity.- R^2 for fraction of variance explained by the common factor.

Important distinction for interpretation:

- High beta does not necessarily imply high R^2.

- A coin can react strongly to market moves on average (high beta), yet still have large idiosyncratic volatility (low R^2).

Coins in the index:

| Ticker | Coin |

|---|---|

| BTC | Bitcoin |

| ETH | Ethereum |

| BCH | Bitcoin Cash |

| LTC | Litecoin |

| XRP | Ripple |

| DOGE | Dogecoin |

| XLM | Stellar |

Sample period used in the code:

- Monthly returns from January 2015 onward (subject to data availability for each asset).

Building a Crypto Market Index

Factor model used for each coin i: r_i = \alpha_i + \beta_i r_{\text{MKT}} + e_i.

MKT is a fixed-weight crypto index (weights based on market-cap shares).

Modeling choice:

- We use fixed weights for transparency and stability of interpretation.

- With time-varying weights, measured beta can mix true exposure changes with index-reweighting effects.

w_raw = pd.Series({

'BTC': 57.5,

'ETH': 11.6,

'XRP': 3.8,

'DOGE': 0.7,

'BCH': 0.4,

'LTC': 0.2,

'XLM': 0.2

})

w = w_raw / w_raw.sum()

weights = pd.DataFrame(np.tile(w.values, (len(df.index), 1)), index=df.index, columns=w.index)

df['MKT'] = (weights * df[w.index]).sum(axis=1)Analyzing the Relationship Between Cryptocurrencies and the Crypto Market Index

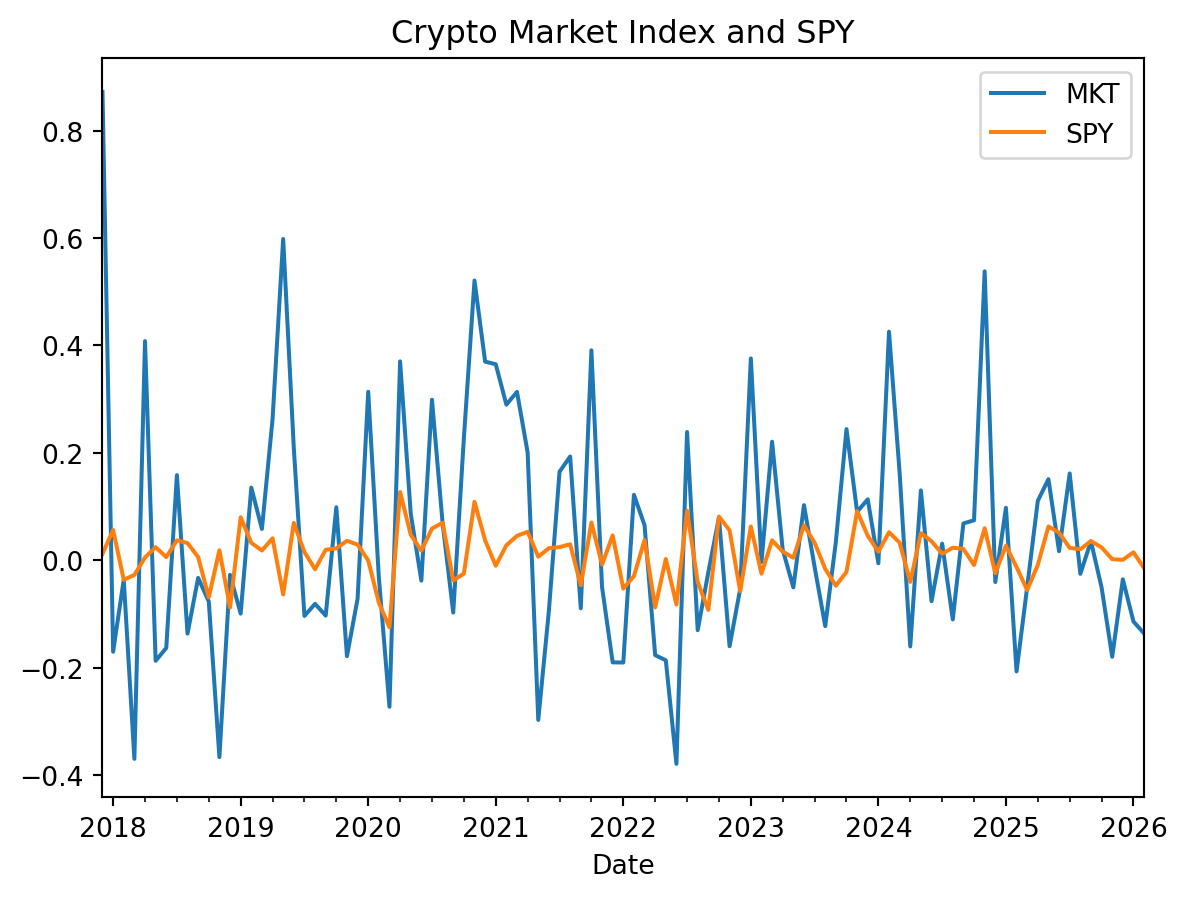

First, we benchmark crypto market volatility against equities:

Key results (in this sample):

- The crypto market index is much more volatile than SPY.

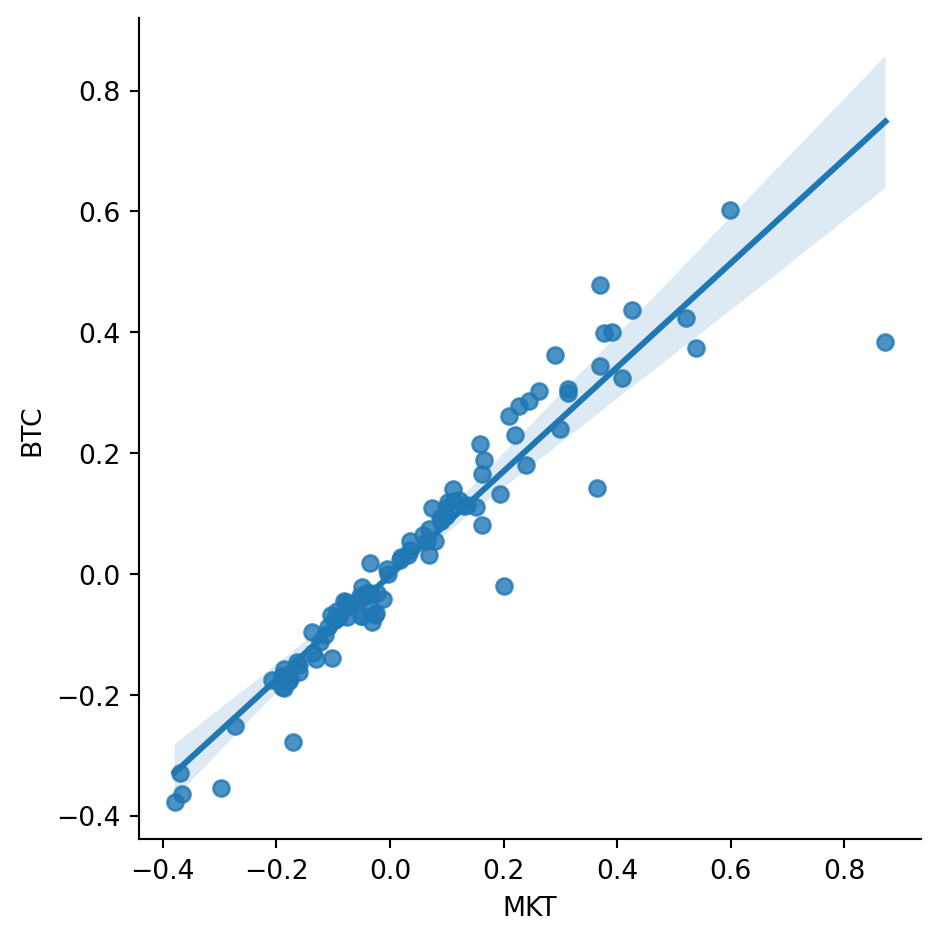

BTC vs MKT

| beta_MKT | p_value(beta=0) | R_squared | |

|---|---|---|---|

| 0 | 0.8612 | 0.0 | 0.9023 |

BTC interpretation:

- BTC has strong positive exposure to the crypto market factor.

- The fit is tight (high R^2), consistent with BTC’s large index weight.

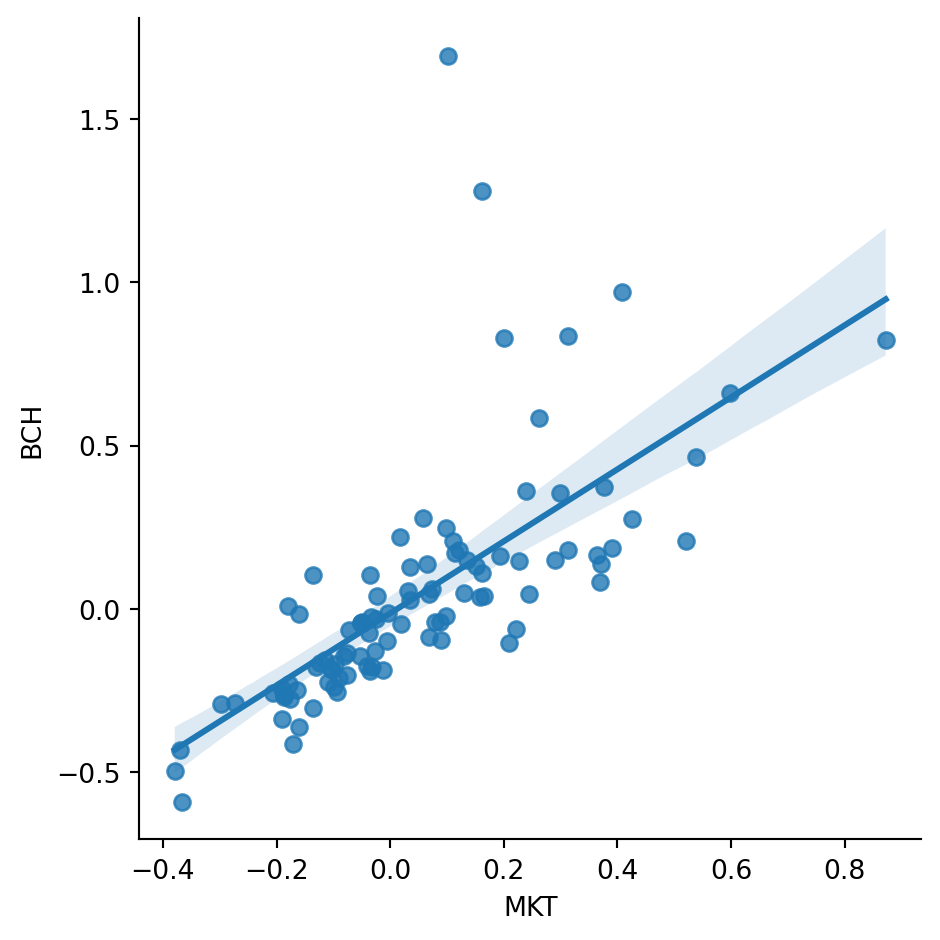

BCH vs MKT

| beta_MKT | p_value(beta=0) | R_squared | |

|---|---|---|---|

| 0 | 1.1018 | 0.0 | 0.4748 |

BCH interpretation:

- BCH still has meaningful market exposure.

- The relationship is noisier than BTC (lower R^2), so more variation is coin-specific.

All Coins on MKT

| Coin | Beta | R-squared | |

|---|---|---|---|

| 7 | MKT | 1.00 | 1.000 |

| 1 | BTC | 0.86 | 0.902 |

| 3 | ETH | 1.08 | 0.721 |

| 4 | LTC | 1.06 | 0.690 |

| 0 | BCH | 1.10 | 0.475 |

| 5 | XLM | 2.07 | 0.433 |

| 6 | XRP | 2.59 | 0.368 |

| 2 | DOGE | 2.13 | 0.229 |

Cross-coin interpretation:

- High beta with low R^2 means strong average market sensitivity but substantial idiosyncratic risk.

- DOGE, XLM, and XRP show relatively high betas but lower R^2, indicating strong average market sensitivity alongside substantial coin-specific risk.

- Sanity check: the

MKTrow should show beta =1 and R^2=1 when regressingMKTon itself.

Statistical reading guide:

- Testing \beta=0: asks whether market exposure is statistically different from zero.

- Confidence intervals: show plausible ranges for true exposure.

- Economic significance (beta size) and statistical significance (p-value) are related but distinct.

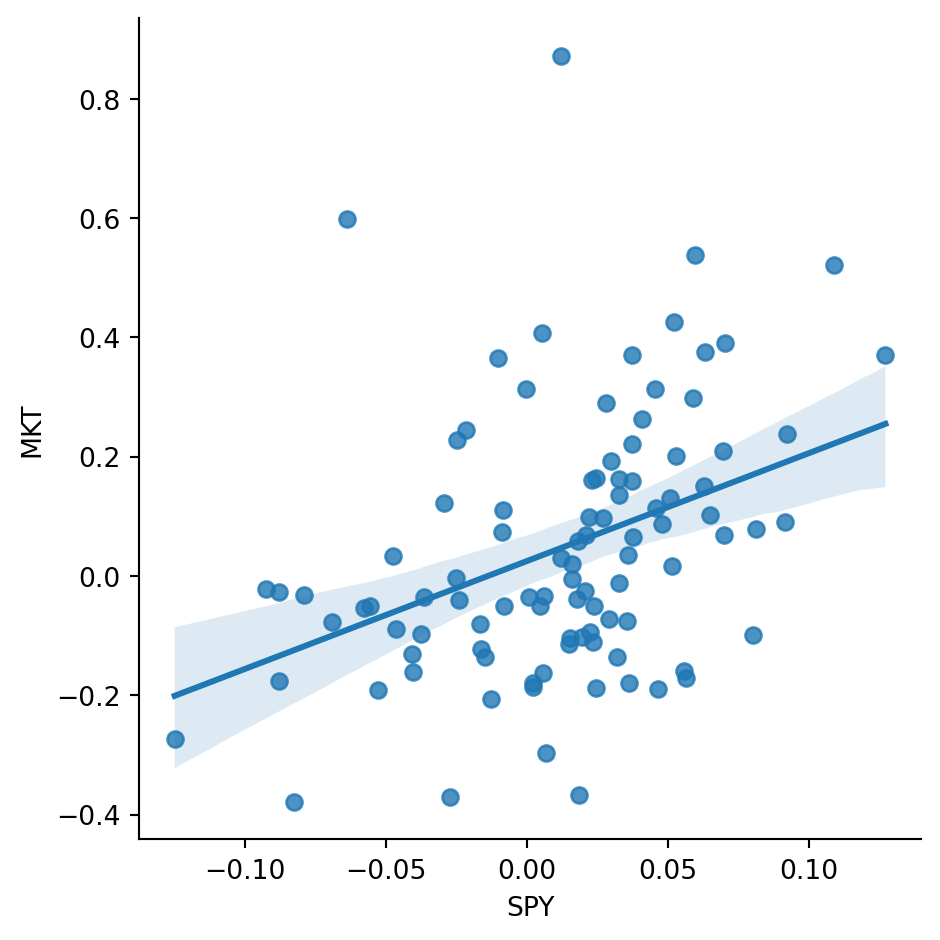

Crypto Market Index vs. Stock Market

Scatter relationship:

| beta_SPY | p_value(beta_SPY=0) | p_value(beta_SPY=1) | R_squared | |

|---|---|---|---|---|

| 0 | 1.8102 | 0.0001 | 0.0682 | 0.1489 |

Key results (in this sample):

SPYloading inMKT ~ SPYis positive and statistically significant (reject \beta_{SPY}=0).- Testing \beta_{SPY}=1: at the 5% level we fail to reject equality to 1, though the result is borderline at the 10% level.

Economic interpretation:

- A positive, significant SPY loading indicates directional co-movement between crypto and equities.

- But R^2 is still crucial: co-movement can be significant while a large share of crypto variation remains unexplained by equities.

Takeaways

- This notebook applies the same regression logic from previous notes to a realistic asset-pricing use case.

Betameasures average market sensitivity; R^2 measures how much variation the market factor explains.- Crypto and equities co-move, but a large share of crypto risk remains crypto-specific.

- Scope note: this notebook is an in-sample modeling exercise (fit and interpretation), not a trading backtest.