import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from scipy.optimize import minimize

import yfinance as yf

import warnings

warnings.simplefilter(action='ignore', category=FutureWarning)

TRAIN_END = '2024-12-31'

TEST_START = '2025-01-01'

MIN_MONTHS = 36

N_TOP = 50Minimum Variance Portfolio

Introduction

Main purpose in this notebook:

- Estimate a minimum-variance equity portfolio in-sample (2020–2024).

- Compare constrained (

No Short) and unconstrained (Short Allowed) solutions. - Evaluate out-of-sample cumulative performance from January 2025 onward.

What we are trying to do, conceptually:

- We are not forecasting returns directly.

- We are choosing weights to minimize estimated portfolio variance, using historical covariance structure.

- Then we test whether that low-variance construction produces better realized risk-adjusted outcomes out-of-sample.

Setup

Build the Universe and Returns Panel

mcap = pd.read_csv('./stocks_mktcap_202412.csv')

tickers = mcap['TICKER'].unique().tolist()

rets = (yf

.download(tickers, start='2020-01-01', progress=False)['Close']

.resample('ME')

.last()

.pct_change()

.dropna(how='all'))

train_rets = rets.loc[:TRAIN_END]

valid = train_rets.count() >= MIN_MONTHS

eligible = mcap.loc[mcap['TICKER'].isin(train_rets.columns[valid])]

top = (eligible.sort_values('MCAP', ascending=False)

.head(N_TOP)['TICKER']

.tolist())

df = rets[top]

train = df.loc[:TRAIN_END]

test = df.loc[TEST_START:].dropna()Data-design note:

- Eligibility is determined using only the training window (

train_rets) to avoid look-ahead bias. - The test sample starts in January 2025 and is not used to estimate weights.

- The

dropna()call in the test panel keeps only months with complete returns for all selected stocks, so the effective out-of-sample window can be shorter than the calendar window.

Estimate Minimum Variance Weights

Optimization problem: \min_{\mathbf{w}}\; \mathbf{w}'\Sigma\mathbf{w} \quad\text{s.t.}\quad \mathbf{1}'\mathbf{w}=1.

Estimation logic:

- Estimate the covariance matrix \Sigma from the training sample.

- Solve the constrained optimization (

No Short). - Solve the unconstrained optimization (

Short Allowed). - Keep weights fixed and evaluate both choices on the test window.

Constraint interpretation:

No Shortimposes 0 \le w_i \le 1, which shrinks extreme positions.Short Allowedremoves box constraints, allowing levered long-short exposures.- In finite samples, the unconstrained solution can overreact to covariance estimation noise.

n = train.shape[1]

cov = train.cov().values

w0 = np.ones(n) / n

objective = lambda w: w @ cov @ w

sum_to_one = {'type': 'eq', 'fun': lambda w: w.sum() - 1}

res = minimize(objective, w0, method='SLSQP', bounds=[(0, 1)] * n, constraints=[sum_to_one])

res_short = minimize(objective, w0, method='SLSQP', constraints=[sum_to_one])Inspect Estimated Weights

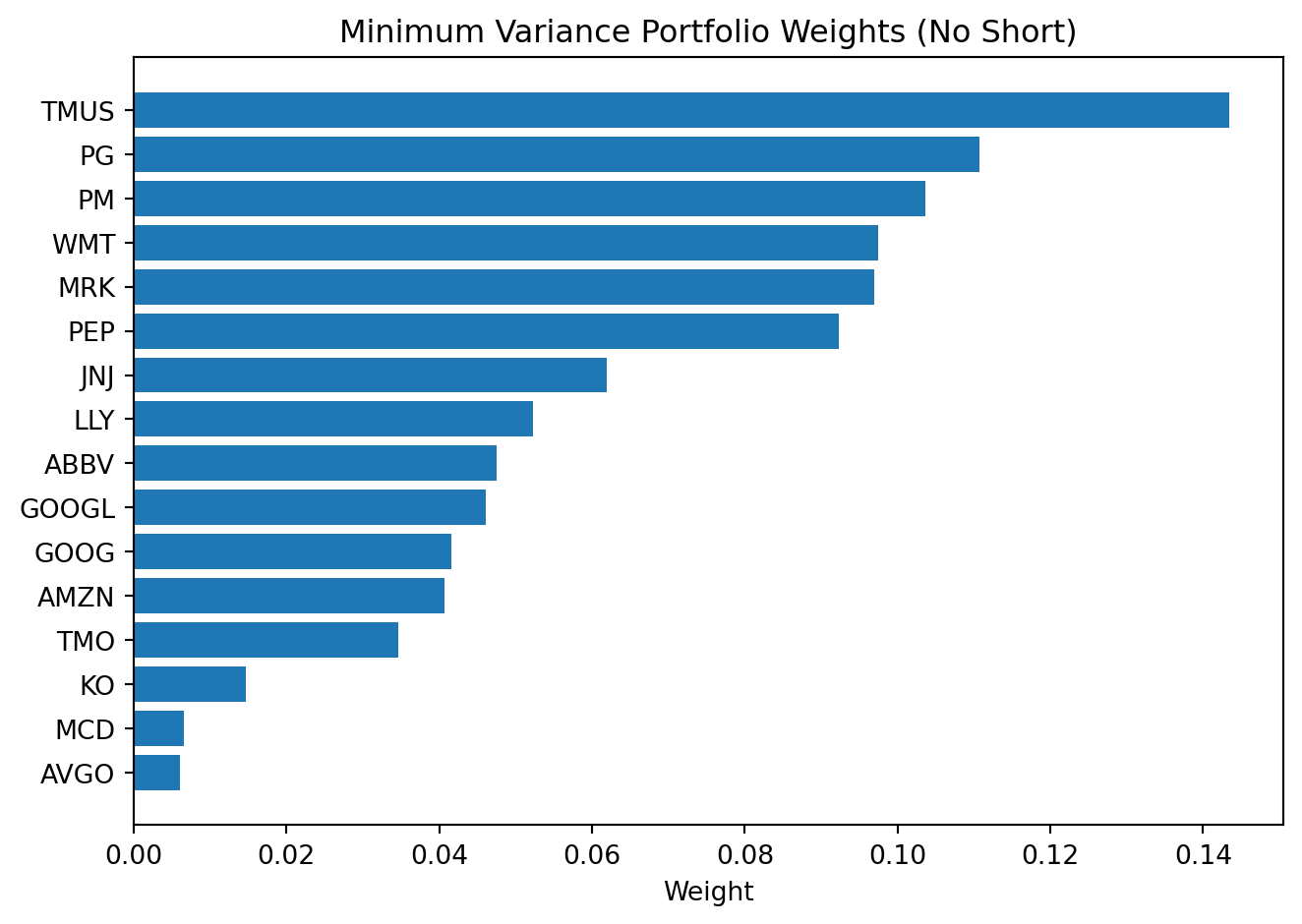

Display filter for the no-short plot:

- Show only holdings with

WEIGHT > 0.5%. - This removes tiny allocations so the chart is readable.

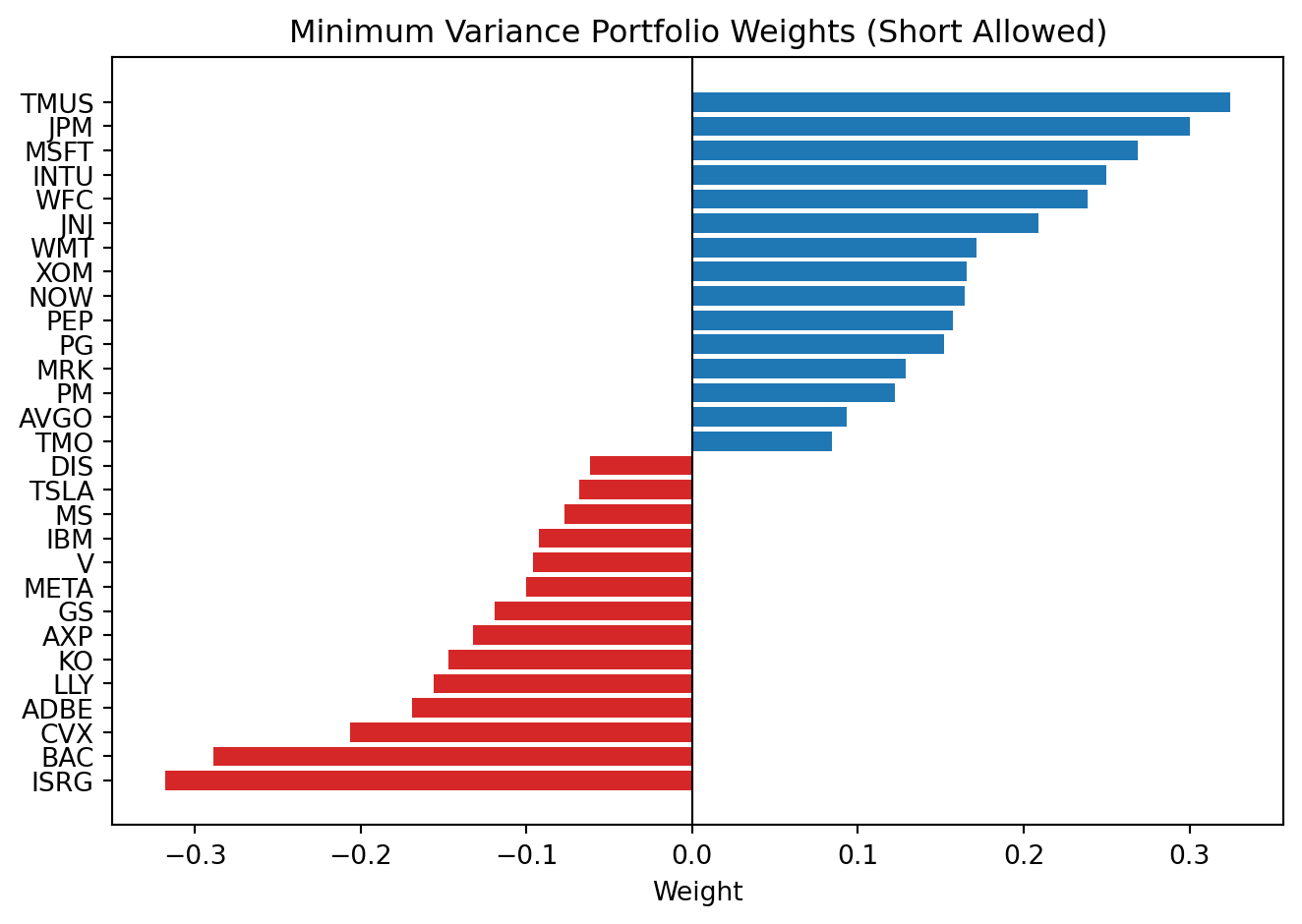

Display filter for the short-allowed plot:

- Show only positions with

abs(WEIGHT) > 6%. - This keeps only economically large long/short positions; smaller offsets are hidden for clarity.

Interpretation:

No Shorttends to produce sparser, more stable allocations.Short Allowedoften creates more extreme positive/negative positions.- Those extremes can look optimal in-sample but may be fragile out-of-sample.

Backtest: January 2025 Onward

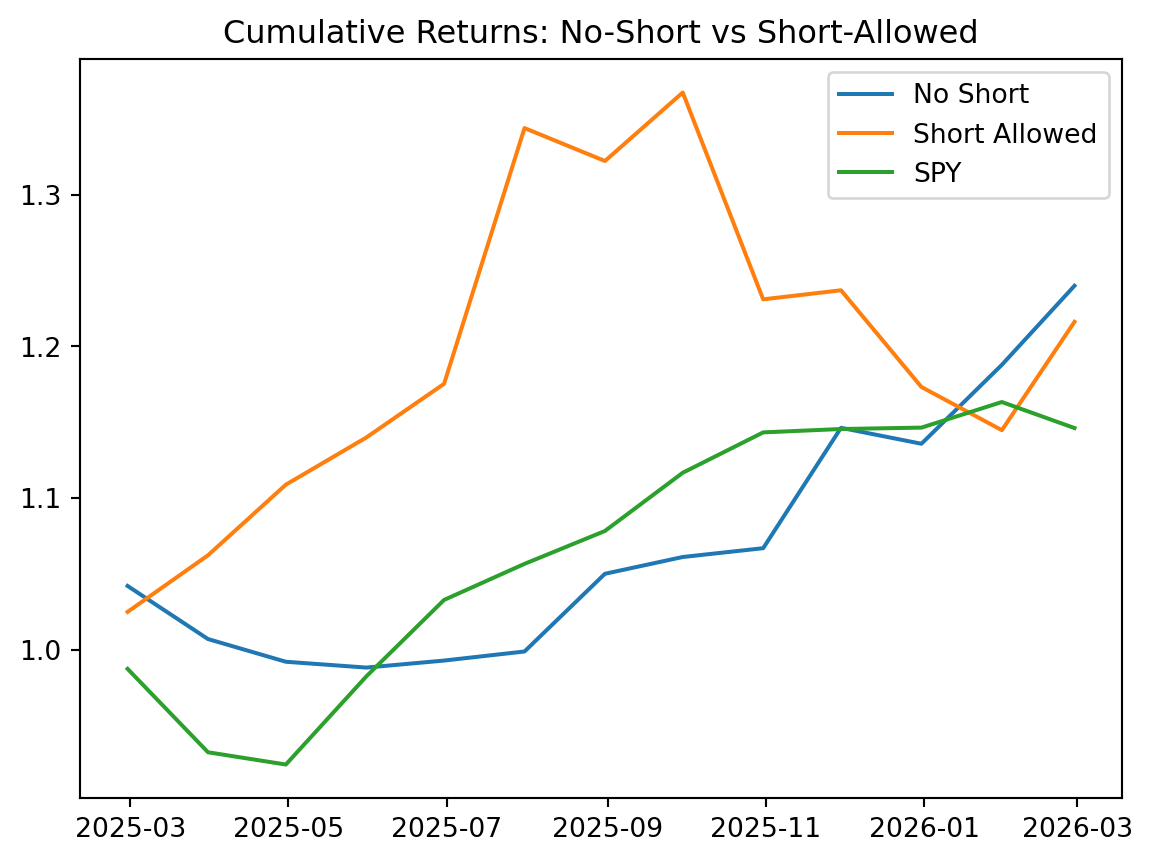

Key result in the notebook sample:

No ShortoutperformsShort AllowedandSPYin this out-of-sample window.- This is consistent with Jagannathan and Ma (2003): in large portfolios, no-short constraints reduce the impact of covariance estimation error by shrinking extreme positions.

- This comparison is based on one realized period, so it is evidence for this sample, not a universal dominance result.

Jagannathan, Ravi, and Tongshu Ma. 2003. “Risk Reduction in Large Portfolios: Why Imposing the Wrong Constraints Helps.” Journal of Finance 58 (4): 1651–83.

How to read the backtest plot:

- Relative slope indicates average realized growth rate over the period.

- Drawdown depth indicates realized risk in stressful months.

- If

No Shortshows smoother growth with smaller drawdowns, that is consistent with a regularization effect: the no-short constraint shrinks extreme covariance-driven weights, reducing sensitivity to covariance estimation error.

Takeaways

- Minimum-variance optimization is highly sensitive to covariance estimation and constraints.

- No-short constraints can improve stability and implementation realism.

- The economic objective is better risk-adjusted performance (Sharpe improvement), not alpha generation. In fact, the expected return of the minimum variance portfolio is typically lower than the market’s — the gain comes from reduced volatility, not higher returns.

- When short-selling is allowed, the optimizer can take on large levered positions that are often unrealistic in practice due to transaction costs, liquidity constraints, and risk management policies. The no-short solution is usually easier and cheaper to implement.

- This notebook is a training/evaluation exercise in one sample period, not a universal portfolio rule.