Quantify slippage, arbitrage alignment, and LP tradeoffs.

Connect AMM mechanics to standard market-microstructure logic.

Market Structure and Motivation

Core contrast:

CEXs mainly use order books (CLOB-style matching).

AMMs execute against pooled reserves and formula-based quotes.

In AMMs, the pool is the immediate counterparty, and price updates through reserve changes (Adams et al. 2020).

Adams, Hayden, Noah Zinsmeister, Moody Salem, River Keefer, and Dan Robinson. 2020. Uniswap V2 Core. Uniswap Whitepaper. https://docs.uniswap.org/whitepaper.pdf.

Constant-Product Pricing

Baseline AMM invariant:

xy=k.

Marginal quote (in y per unit of x):

P=\frac{y}{x}.

import numpy as npimport pandas as pdimport matplotlib.pyplot as pltx0 =1_000.0y0 =1_000.0k = x0 * y0def cp_swap_buy_x(delta_y, x=x0, y=y0): y_new = y + delta_y x_new = k / y_new dx_out = x - x_new avg_price = delta_y / dx_outreturn {"delta_y_in": delta_y,"x_out": dx_out,"avg_price": avg_price,"marginal_before": y / x,"marginal_after": y_new / x_new, }trades = pd.DataFrame([cp_swap_buy_x(dy) for dy in [10, 50, 100, 200, 400]])trades.round(4)

delta_y_in

x_out

avg_price

marginal_before

marginal_after

0

10

9.9010

1.01

1.0

1.0201

1

50

47.6190

1.05

1.0

1.1025

2

100

90.9091

1.10

1.0

1.2100

3

200

166.6667

1.20

1.0

1.4400

4

400

285.7143

1.40

1.0

1.9600

Key interpretation:

Larger trades move price more (endogenous impact), analogous to walking the book.

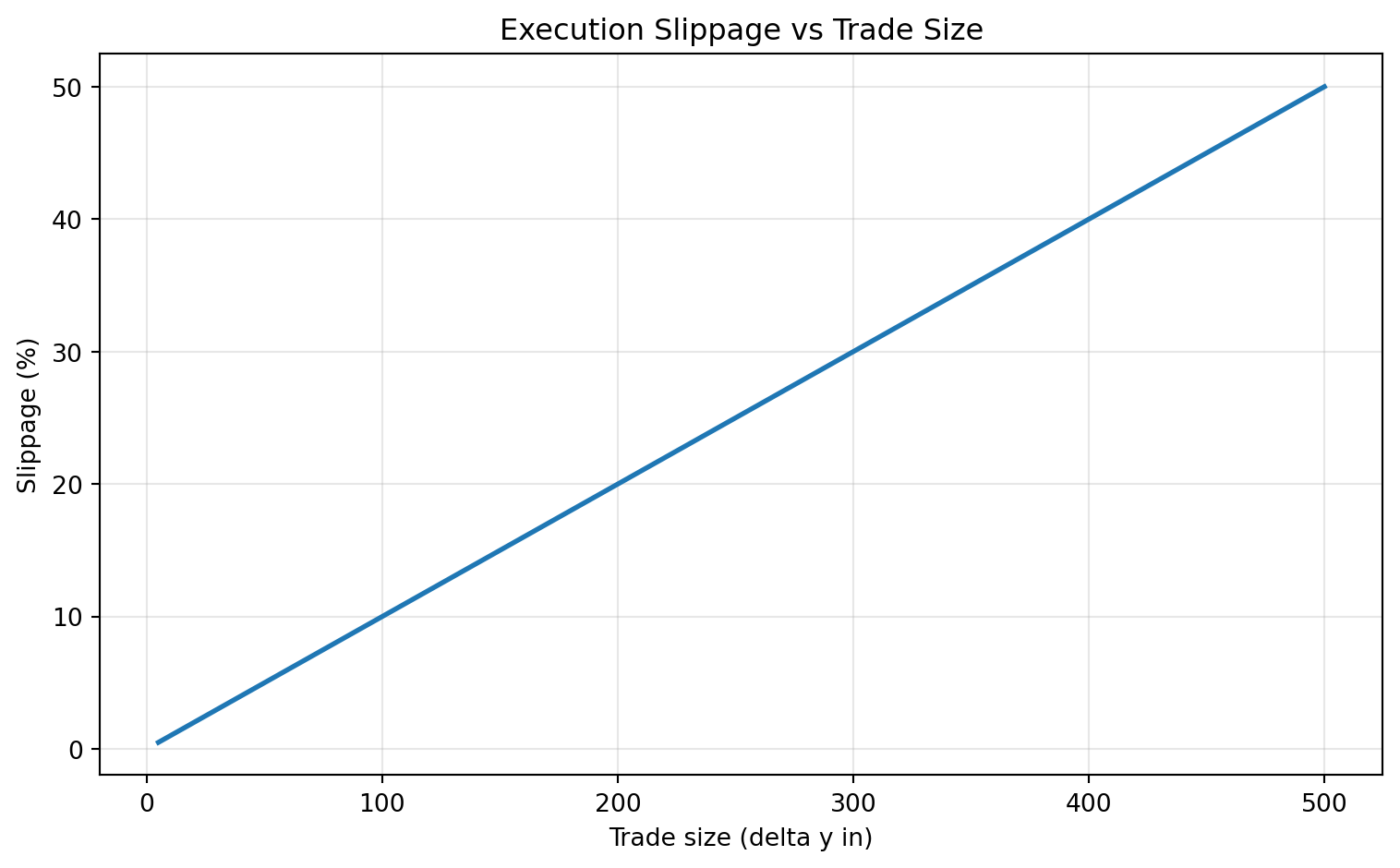

Slippage and Trade Size

Slippage metric used in the notebook:

\text{slippage}=\frac{P_{\text{avg}}}{P_{\text{pre}}}-1.

Key result:

Slippage rises nonlinearly with trade size relative to pool depth.

Arbitrage and Price Alignment

When external price is P^*, no-fee aligned reserves satisfy:

\frac{y}{x}=P^*,\quad xy=k,

so

x=\sqrt{\frac{k}{P^*}},\qquad y=\sqrt{kP^*}.

p_external

x_reserve

y_reserve

pool_price

0

0.8

1118.0340

894.4272

0.8

1

1.0

1000.0000

1000.0000

1.0

2

1.2

912.8709

1095.4451

1.2

3

1.5

816.4966

1224.7449

1.5

Key interpretation:

AMM prices adjust via arbitrage flow; reserves transmit external information into on-chain prices (Capponi et al. 2026).

Capponi, Agostino, Ruizhe Jia, and Shuo Yu. 2026. “Price Discovery on Decentralized Exchanges.”Review of Financial Studies, ahead of print. https://doi.org/10.1093/rfs/hhag002.

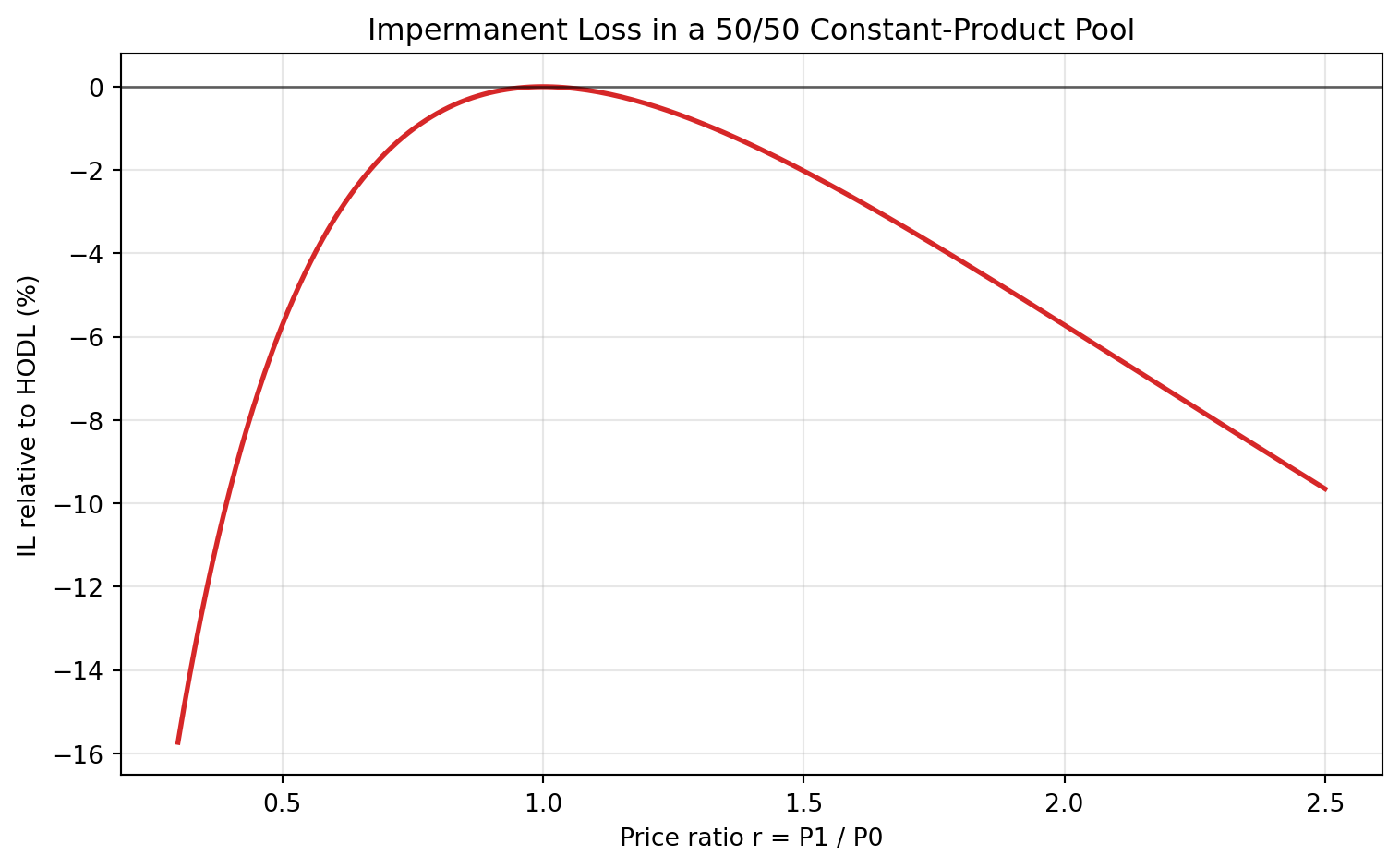

LP Fees vs Impermanent Loss

Impermanent loss (IL) benchmark in a 50/50 pool:

\mathrm{IL}(r)=\frac{2\sqrt r}{1+r}-1,

\qquad r=\frac{P_1}{P_0}.

Fee income benchmark:

\text{LP fee income} \approx s\,f\,V,

where s is LP share, f fee rate, V traded notional.

Key interpretation:

LP outcomes depend on fee income versus volatility-driven inventory drift (IL) (Capponi et al. 2025).

Capponi, Agostino, Ruizhe Jia, Yubo Ma, John Wang, and Boyu Zhu. 2025. “Liquidity Provision on Blockchain-Based Decentralized Exchanges.”Review of Financial Studies 38 (10): 3040–85. https://doi.org/10.1093/rfs/hhaf046.

How Uniswap v3 and v4 Differ from This Notebook

Notebook baseline is v2-style full-range liquidity.