import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import yfinance as yf

import seaborn as sns

import warnings

warnings.simplefilter(action='ignore', category=FutureWarning)Introduction to Jupyter Notebooks

Introduction

Main purpose in this notebook:

- Introduce the Python workflow used in class.

- Download and transform finance data with

yfinanceandpandas. - Visualize co-movement and volatility differences with simple plots.

Libraries

Data and Returns

df = (yf

.download(['MSFT', 'SPY'], progress=False, start='2000-01-01')

.loc[:, 'Close']

.resample('ME')

.last()

.pct_change())Sample period used in the code:

- Monthly returns from January 2000 onward (subject to data availability).

Return Comparison

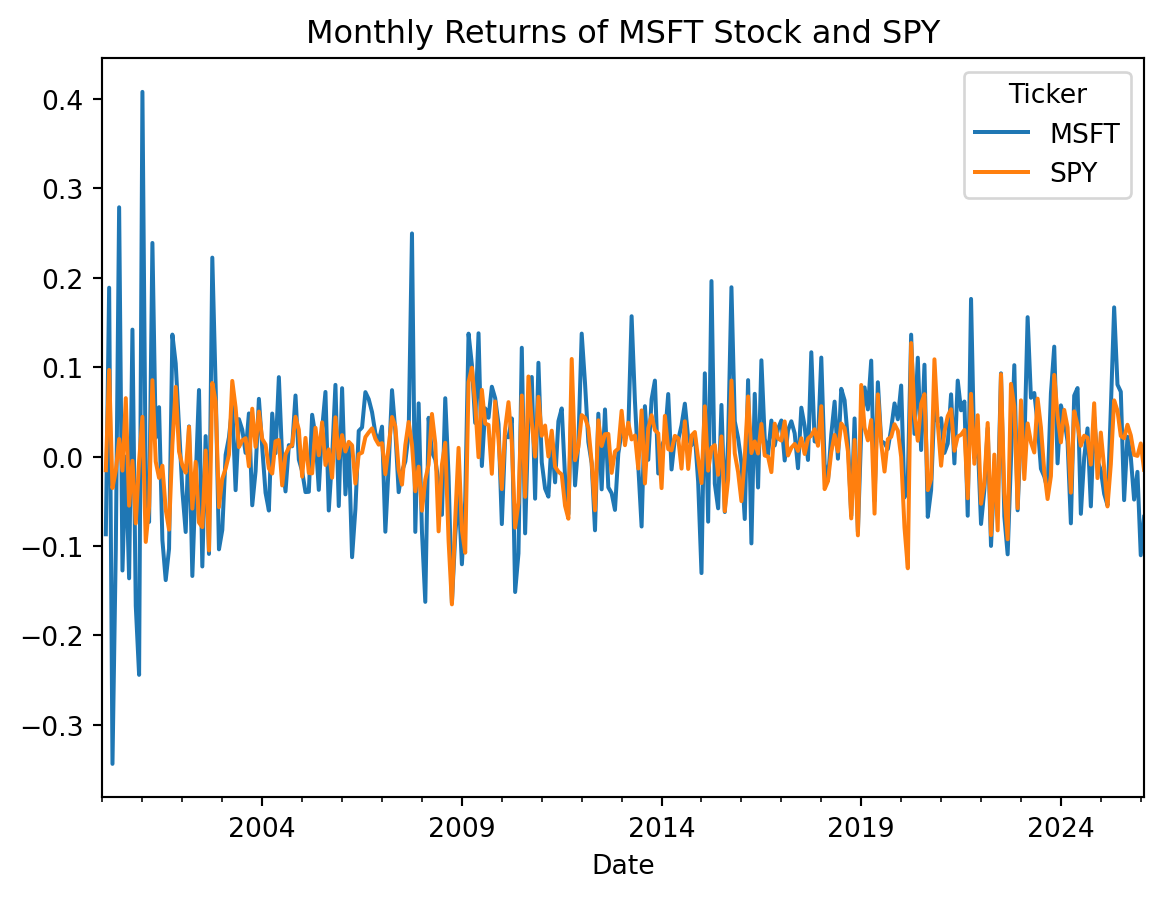

df.plot(title='Monthly Returns of MSFT Stock and SPY')

Key result:

SPYreturns are less volatile thanMSFTreturns, consistent with index diversification.

Co-Movement View

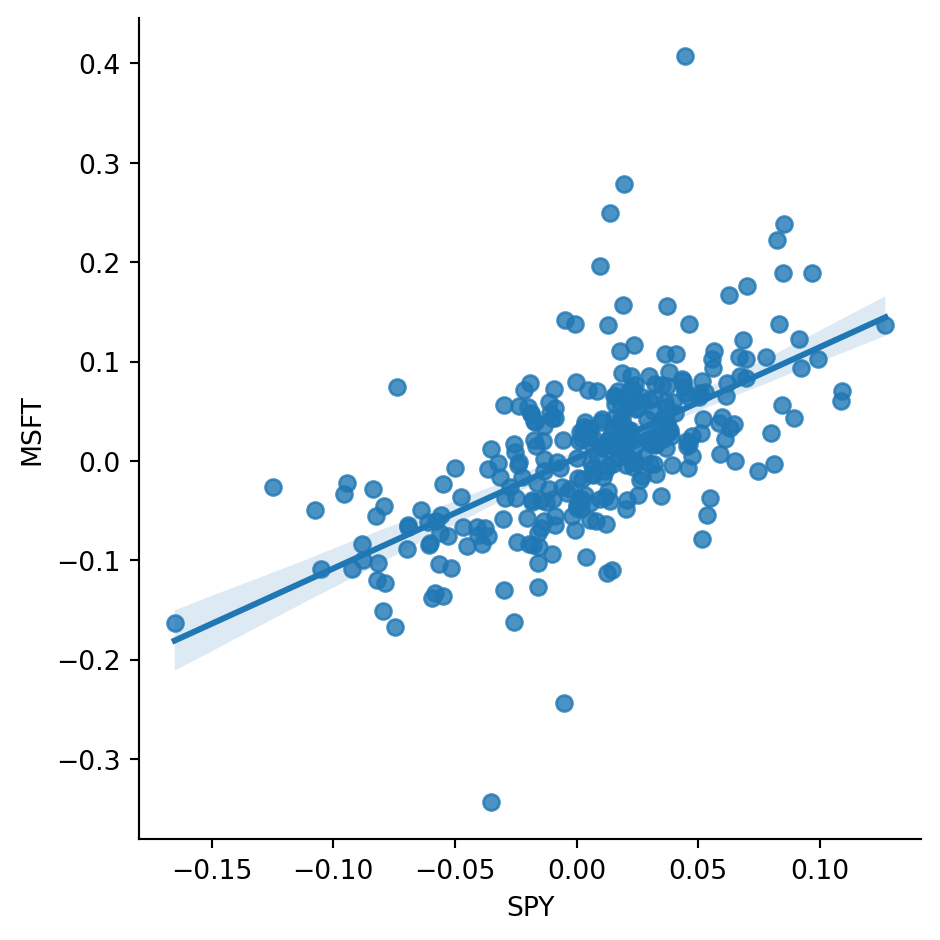

sns.lmplot(data=df, x='SPY', y='MSFT')

Interpretation:

MSFTandSPYshow clear positive co-movement.- This visual relationship motivates factor-style regressions used later in the course.

Takeaways

yfinance+pandas+ plotting tools are enough for a complete first empirical workflow.- The key steps are: download data, resample, compute returns, and interpret basic diagnostics.

- This notebook is a setup notebook; it introduces tools rather than advanced model testing.