OLS Regression Results

==============================================================================

Dep. Variable: RETRF R-squared: 0.632

Model: OLS Adj. R-squared: 0.631

No. Observations: 372 F-statistic: 634.4

Covariance Type: nonrobust Prob (F-statistic): 3.03e-82

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 0.0043 0.002 2.282 0.023 0.001 0.008

RMRF 1.0445 0.041 25.187 0.000 0.963 1.126

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

The CAPM alpha is positive (a = 0.0043) and statistically significant at the 5% level (p-value = 0.023), so the fund outperformed the market after adjusting only for market exposure.

After controlling for the other factors, the alpha is positive (a = 0.0027) but only marginally significant at the 10% level (p-value = 0.094). In other words, the fund outperformed by 0.27 \times 12 = 3.24\% per year after controlling for systematic factors, though this result is not statistically significant at conventional levels.

Factor

Coefficient

Significance

Interpretation

SMB

0.3163

1%

The fund invested in small stocks

HML

0.3767

1%

The fund invested in value stocks

RMW

0.2921

1%

The fund invested in stocks with strong profitability

CMA

0.1150

Not significant

The fund invested in both high and low investment stocks

MOM

-0.1049

1%

The fund was significantly contrarian by chasing losers

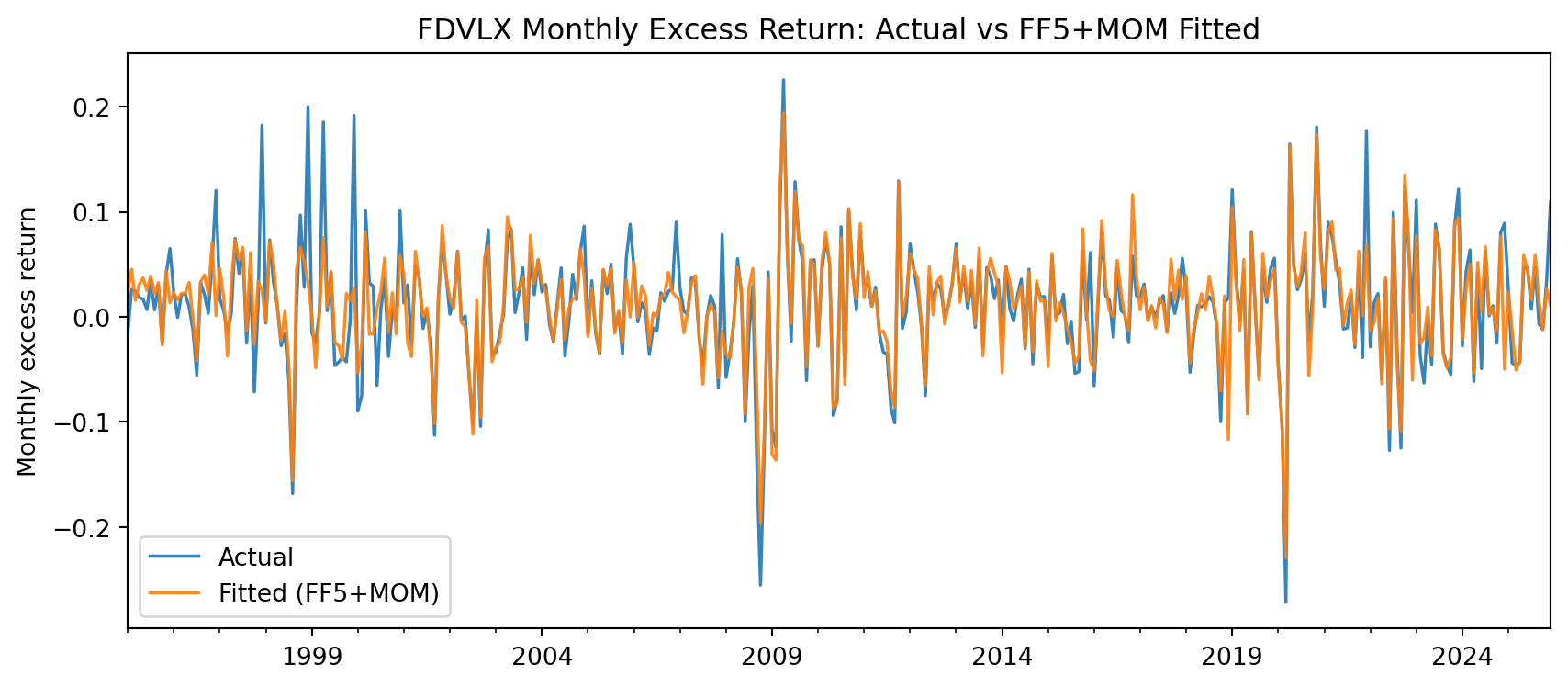

Fit Check (Actual vs Fitted Excess Return)

The next plot compares realized excess returns against fitted values from the augmented model.

The results from the regression broadly agree with the fund description. The exposure to SMB is positive, even though Morningstar categorizes the fund as Mid-Cap Value. The fund returns load significantly on HML, which is consistent with the fund being a value fund. The negative exposure to momentum may come from the fact that value firms often have low P/E ratios, which commonly occur after stock price declines. After controlling for all these systematic exposures, alpha is positive but not statistically significant at conventional levels in this sample.

Takeaways

Performance evaluation should control for multiple risk factors, not only market beta.

Alpha interpretation changes with model specification.

Factor regressions are a practical tool for diagnosing how a fund earns returns.