import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

import torch

import torch.nn as nn

from torch.utils.data import DataLoader, TensorDataset

from sklearn.model_selection import train_test_split

from sklearn.preprocessing import StandardScaler

from sklearn.metrics import mean_absolute_error, r2_score

import yfinance as yf

seed = 420

np.random.seed(seed)

torch.manual_seed(seed)

device = torch.device("cuda" if torch.cuda.is_available() else "cpu")

df = pd.read_csv("./108105_2023_C_options_data.csv")

df["date"] = pd.to_datetime(df["date"])

vix = yf.download("^VIX", start="2023-01-01", progress=False, multi_level_index=False)[["Close"]]

vix.columns = ["^VIX"]

df = df.merge(vix, left_on="date", right_index=True, how="left")

cleaned_df = df[["S", "K", "T", "^VIX", "Impl_Vol"]].copy()

cleaned_df = cleaned_df.dropna(subset=["S", "K", "T", "^VIX", "Impl_Vol"])

cleaned_df = cleaned_df[(cleaned_df["Impl_Vol"] < 0.6) & (cleaned_df["T"] > 29) & (cleaned_df["T"] < 681)]

cleaned_df["moneyness"] = cleaned_df["K"] / cleaned_df["S"]

cleaned_df = cleaned_df[cleaned_df["moneyness"] > 0.1]Volatility Surface Modeling with Neural Networks

Introduction

Main purpose in this notebook:

- Apply the same ML fitting logic to real SPX option data.

- Predict implied volatility (IV) from option and market features.

- Evaluate fit quality and compare observed vs predicted IV surfaces.

What we are trying to do, conceptually:

- Here, implied volatility (IV) is the volatility value that, when plugged into an option-pricing model (typically Black-Scholes), matches the market option price.

- So IV is not directly observed like price or volume; it is implied from observed option prices.

- In options markets, IV is not flat; it varies across moneyness and maturity (the IV surface).

- Instead of imposing a rigid parametric shape, we train a neural network to learn the mapping \text{IV} = f\big(\text{moneyness}, T, S, \text{VIX}\big).

- Economically, this is a nonlinear interpolation/extrapolation problem: use historical cross-sections of options to learn a surface that captures level, slope, and curvature patterns in market IV.

- The goal is approximation quality of the observed surface, not structural causal identification.

Scope note:

- This is a modeling workflow focused on approximation quality, not on trading performance.

- Evaluation uses a random held-out test split within the same sample period (not a forward-time backtest).

Data Loading and Preprocessing

Core features used:

- K/S (moneyness)

- T (days to maturity)

- S (spot level)

VIX(market-wide volatility state)

Filter logic:

- Keep observations in a practical IV/maturity region used in class.

- This improves stability and avoids extreme points dominating the fit.

Model Training

Training logic in detail:

- Build supervised-learning inputs and target: X = (K/S,\; T,\; S,\; \text{VIX}),\qquad y = \text{Impl\_Vol}.

- Split into train and test sets so evaluation is on held-out observations relative to the fitted parameters.

- Standardize features using training data only. This avoids scale dominance (for example, raw S vs normalized moneyness) and prevents test-set leakage.

- Use a feedforward neural network with ReLU activations:

- hidden layers transform inputs into nonlinear features,

- final layer maps those features to one scalar prediction (IV).

- Minimize mean squared error (MSE) with Adam: \min_{\theta} \frac{1}{N}\sum_{i=1}^N\big(\hat y_i(\theta)-y_i\big)^2. Backpropagation computes gradients of this objective, and Adam updates parameters iteratively.

- Repeat over epochs:

- each epoch passes through minibatches of training data,

- each minibatch step updates parameters to reduce prediction error.

Training note:

train_size=0.01means only 1% of the sample is used for training (chosen for speed in class/demo settings).- With larger training fractions, fit quality is typically higher but run time increases.

- Using a small train fraction makes this notebook a fast demonstration of workflow; for production modeling, you would usually use much more training data and more formal validation/tuning.

Model Evaluation

Evaluation goal:

- Check not only average error size, but also where errors concentrate and whether the model preserves cross-sectional structure.

- A useful evaluation in options problems is multi-layered:

- scalar metrics (MAE/RMSE/R^2),

- local diagnostics (error vs moneyness),

- calibration diagnostics (predicted vs observed levels).

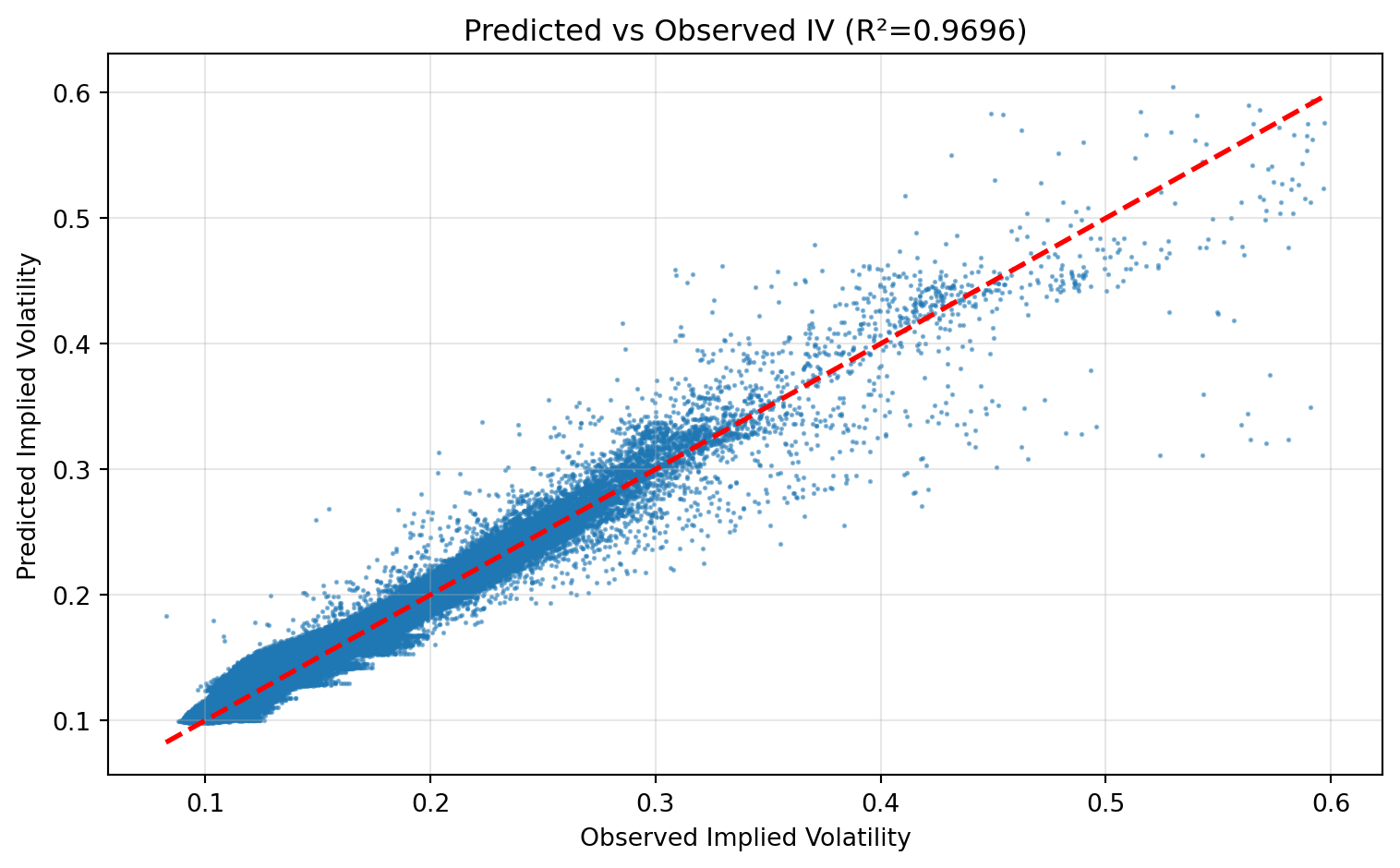

| MAE | RMSE | R_squared | |

|---|---|---|---|

| 0 | 0.004622 | 0.006905 | 0.96959 |

How to read these metrics:

MAE: average absolute IV error (easy to interpret in IV points).RMSE: penalizes larger errors more than MAE.- R^2: fraction of IV variation explained by the model on the test sample.

Interpretation guide:

- If RMSE is much larger than MAE, a small subset of observations likely has large errors.

- A high R^2 with nontrivial MAE can still occur when the model gets relative ranking right but misses absolute levels in some regions.

- Because IV has regime and moneyness structure, aggregate metrics alone are not enough.

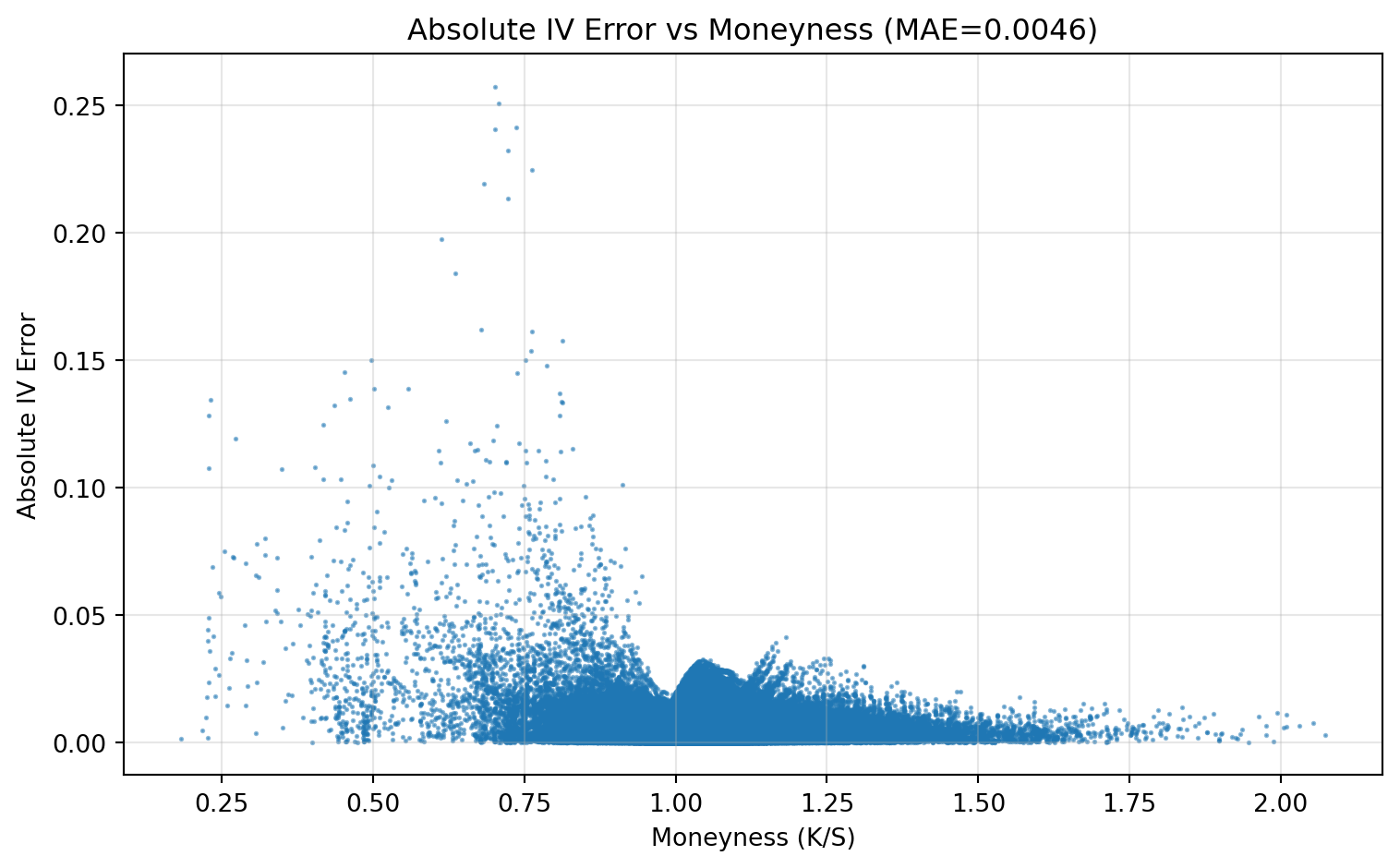

What this plot checks:

- Whether errors are systematically larger in specific moneyness regions (for example deep OTM/ITM).

- Ideally, points should be low and roughly pattern-free; clear bands or slopes indicate model misspecification in that region.

What this plot checks:

- Points near the 45-degree line indicate good calibration.

- Curvature away from the line indicates bias (overprediction/underprediction in parts of the IV range).

- Fan-shaped dispersion indicates heteroskedastic errors (error variance grows with IV level).

Key result:

- The model captures a substantial part of IV variation in this sample, with visible but non-uniform residual error.

Visualizing the Volatility Surface

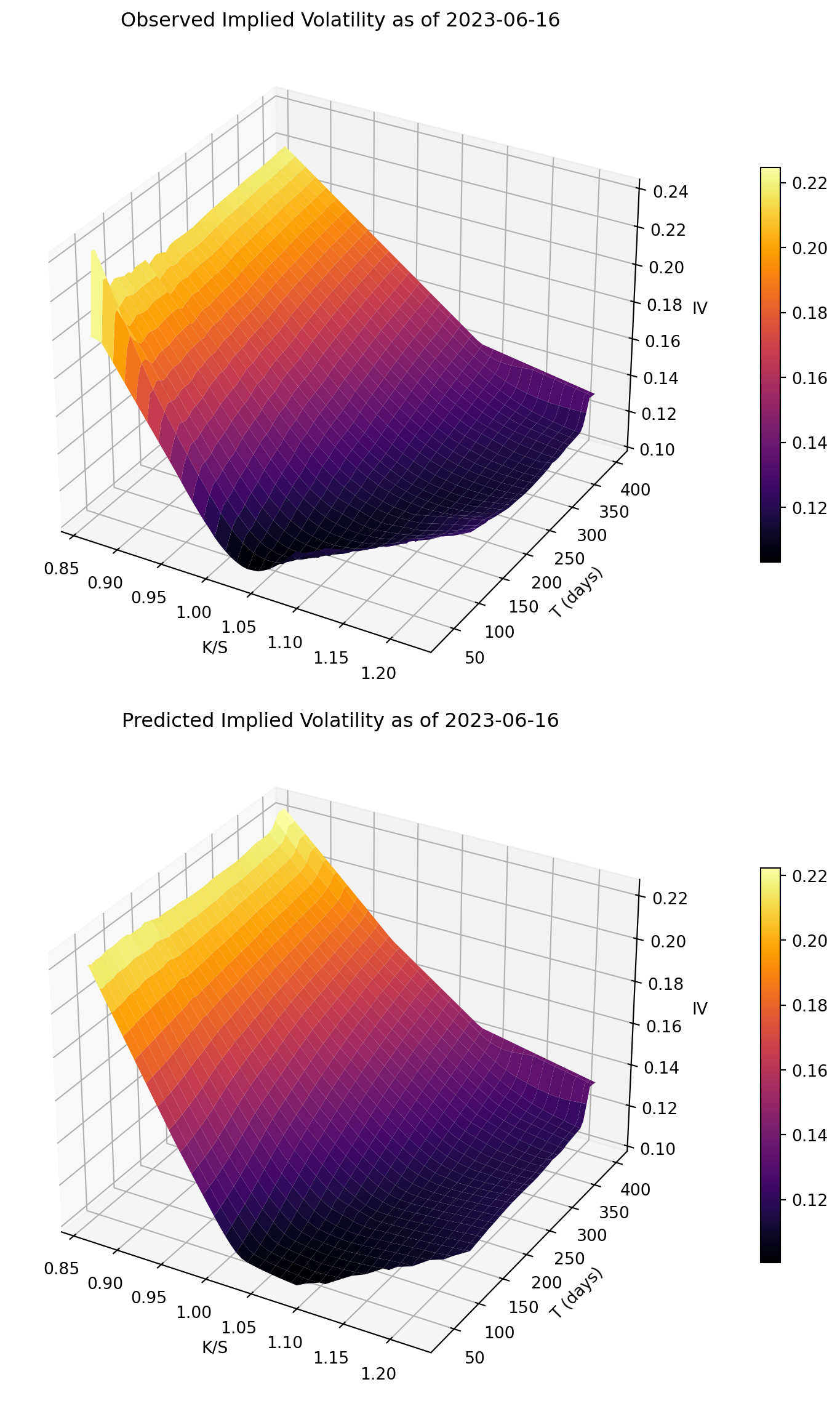

Surface-plot interpretation:

- The objective is shape matching: level, slope, and curvature across moneyness and maturity.

- Good visual agreement supports the idea that the network learned the main surface structure.

Key result:

- The predicted surface broadly reproduces the observed level and shape on the target day.

Takeaways

- This notebook applies the same training/fit/evaluation framework to real options data.

- IV prediction quality should be judged both statistically (MAE/RMSE/R^2) and visually (surface shape).

- Scope note: this is an ML modeling exercise with a random held-out test split, not a trading strategy backtest.